Soda: Returning to Supply and Demand after Emotion

Written date: October 31, 2024

Metal department

Name Zhang Xi

QualificationNo.: F3046164

Investment consulting number: Z0015768

abstract

At present, the soda ash disk is rising with the glass, and the varieties of real estate departments are rising in the short term, which has boosted the soda ash market. From a fundamental point of view, soda ash is still surplus. Even after the production reduction, the inventory hit a new high in the year, and the current inventory is close to the highest level in history. Lianyungang Alkali Industry, Debon, Xiangyu Salt Chemical Industry and Zhongtian Alkali Industry with a total capacity of 2.3 million tons are expected to reach full production in the fourth quarter, and the supply pressure is still relatively high. Recently, the export orders of soda ash are general, and the increase of sea freight is superimposed on the loosening of foreign prices, and the export performance of soda ash is dull.

On the whole, the upward elasticity of prices is limited before the supply and demand ends have improved significantly. In view of the good macro atmosphere in the short term, it is necessary to be alert to the influence of marginal improvement of commodity sentiment on the price trend of soda ash.

Risk warning: investors and production enterprises need to pay close attention to supply changes and the rhythm of downstream replenishment in order to make reasonable business decisions.

First, the spot market analysis.

In terms of spot, the domestic soda ash spot market fluctuated and the price was adjusted within a narrow range. Short-term stoppage or equipment problems of individual enterprises have led to a narrow decline in start-up and output.

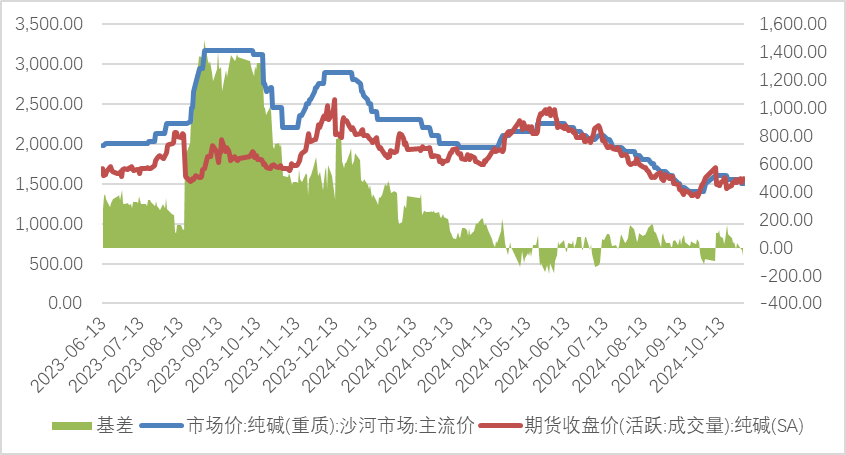

In terms of futures, the price of soda ash continued to fluctuate. At present, the futures premium is high, and the delivery price in the mainstream area is 1450-1500 yuan/ton, and the disk is temporarily supported in this position. If soda ash is started at a high level, there is still room for downward price.

Figure 1: Basis difference of soda ash (yuan/ton)

Figure 2: chart of main contract of soda ash futures (yuan/ton)

Source: Steel Union Data, Wenhua Finance, Huishang Futures Research Institute.

Second, the analysis of supply and demand and its influencing factors

(1) The downward trend of the supply side continues.

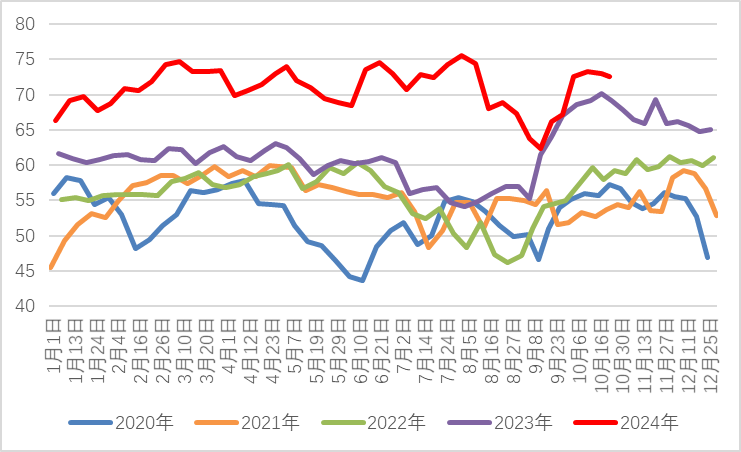

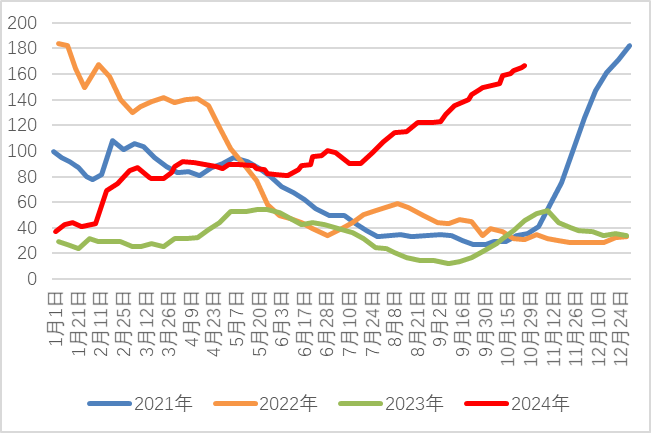

Since the load of Shandong Haitian dropped last week, Tangshan Sanyou Equipment announced the reduction to about 70% at the beginning of this week. As of October 25, 2024, the overall operating rate of soda ash was 87.11%, a decrease of 0.44% from the previous month and an increase of 1.77% from the same period last year. The output of soda ash in Zhou Du was 726,100 tons, a decrease of 0.5% from the previous month and an increase of 5.23% year-on-year. From the seasonal trend chart, we can see that the operating rate of soda ash has decreased greatly recently, which is close to the historical average level. From the absolute value of the operating rate, about 80% of the operating rate is still in line with the balanced expectation. As long as the operating rate is maintained at a high level, the fundamentals will remain weak.

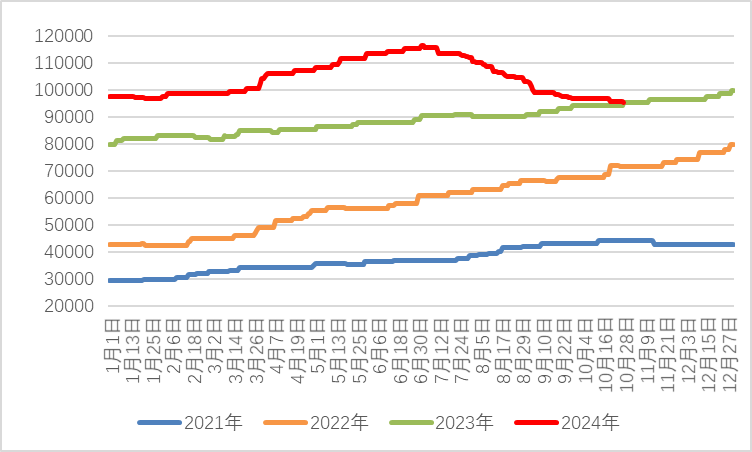

Judging from the seasonal trend of output, the weekly output of soda ash is still at a high level over the years. In the early stage, due to the continuous drop in spot prices, the pace of overhaul and load reduction in some soda plants has been accelerated, and the overall output has been reduced. At present, it has returned to a high level of operation, and the upward pressure on soda ash prices still exists.

Figure 3: Seasonal trend chart of domestic soda ash production (10,000 tons)

Figure 4: Seasonal trend chart of operating rate of soda ash (%)

Source: (), Huishang Futures Research Institute

(B) raw material demand support is weak

At present, the float glass fueled by natural gas and coal-to-gas is in a state of loss, and the average weekly profit of float glass fueled by petroleum coke reaches 30.99 yuan/ton. There are many water discharge plans in the production line. Although some production lines have ignition plans, there is no glass output, so the overall output may show a downward trend.

The demand for float glass and photovoltaic glass has weakened, and the increase in industry losses has led to a gradual contraction in glass production capacity. As of October 28, 2024, the domestic float glass production capacity was 159,700 tons/day according to the statistics of the Steel Federation, a decrease of 2.29% from the previous month and a decrease of 7.01% from the same period last year. The production capacity of photovoltaic glass was 95,300 tons/day, a decrease of 0.7% month-on-month and 0.27% year-on-year.

According to the statistics of the Steel Federation, the operating rate of domestic float glass was 78.52%, up 0.28% from the previous month and down 3.89% from the same period of last year, and the number of production lines started was 234.

On the whole, the cold repair has been carried out slowly. Since March, the number of production lines has been reduced by 25, the overall supply has been tightened, the heavy caustic soda just needs to be reduced, and the demand side is weak in supporting the market.

Figure 5: Seasonal trend chart of daily melting amount of float glass (ton)

Figure 6: Seasonal trend chart of daily melting amount of photovoltaic glass (ton)

Source: Straight Flush and Huishang Futures Research Institute.

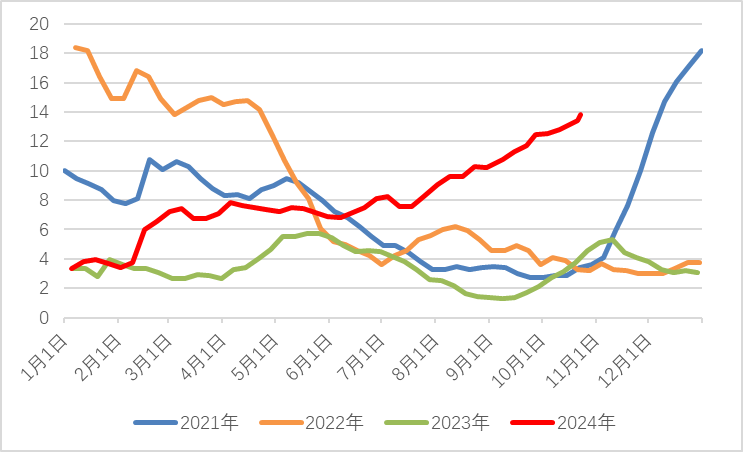

(3) Inventories hit a new high in the year.

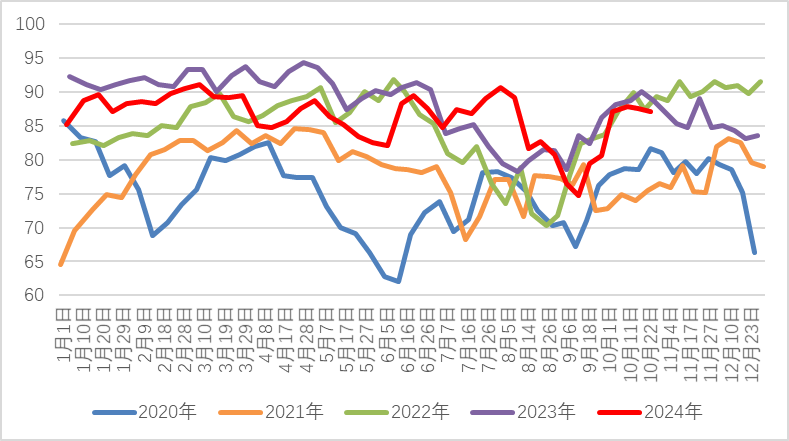

At present, under the influence of the weak downstream demand of soda ash and the mentality of buying up but not buying down, the recent market sentiment is depressed, and the orders of soda plants are generally received. Most of the inventory in the early stage has been transferred to the middle reaches, and the upstream begins to return to the accumulation process. As of October 25, 2024, the total inventory of domestic soda ash manufacturers was 1.663 million tons, an increase of 0.77% from the previous month and 266.46% from the same period last year.

At present, the accumulation of soda plants continues, and the continuous high inventory weakens the upward kinetic energy of soda ash prices to some extent. Short-term observation of production reduction shows that in the case of sustained losses, high-cost producers may potentially reduce their burdens, and the inventory pressure may be eased.

Figure 7: Seasonal trend chart of soda enterprise inventory (10,000 tons)

Figure 8: Seasonal trend chart of available days of inventory (days)

Source: Straight Flush and Huishang Futures Research Institute.

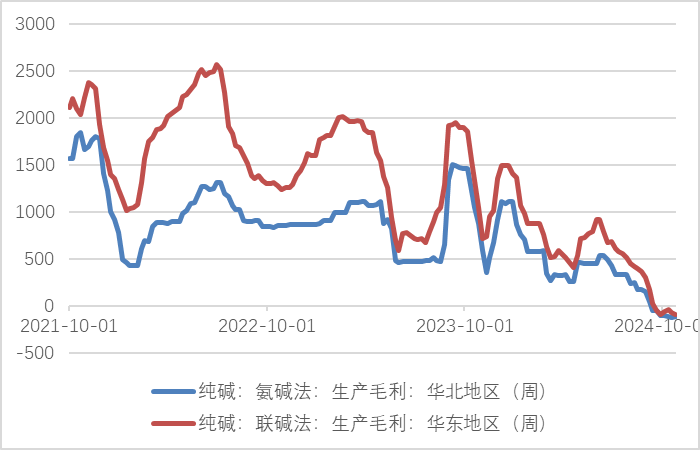

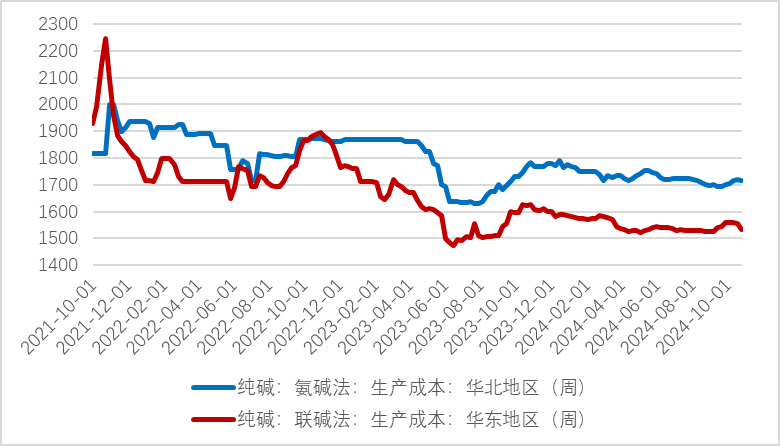

(D) The profit of ammonia-alkali combined alkali is negative.

This round of decline in soda ash market began in May, breaking through the tradition of seasonal fluctuation in previous years. In the peak season, the price center of soda ash market continued to move down from July to August, and the profitability of enterprises continued to deteriorate, and the overall profit was far lower than the historical level. As of October 25th, 2024, the production profit of domestic ammonia-alkali enterprises was -116.5 yuan/ton, down by 3.26% month-on-month and 119.67% year-on-year. The production profit of combined alkali enterprises was -87.9 yuan/ton, down by 36.49% month-on-month and down by 112.17% year-on-year.

The consumption of materials in ammonia-alkali process is mainly synthetic ammonia, coal, salt and limestone, while the main materials in combined alkali process are coal and salt. At present, the average cost is slightly higher than that of the same period last year. According to the statistics of Flush Information, the cost of domestic ammonia-alkali enterprises is 1,717 yuan/ton, down 0.17% from the previous month and 2.87% from the same period last year. The cost of the combined alkali enterprise was 1,532.87 yuan/ton, down 1.32% from the previous month and 4.72% from the same period last year.

Figure 9: Profit of soda ash (yuan/ton)

Figure 10: Cost of soda ash (yuan/ton)

Source: Straight Flush and Huishang Futures Research Institute.

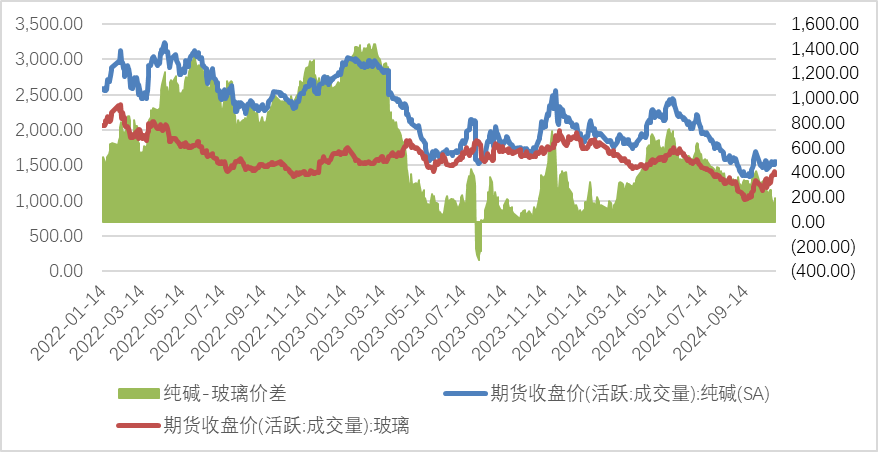

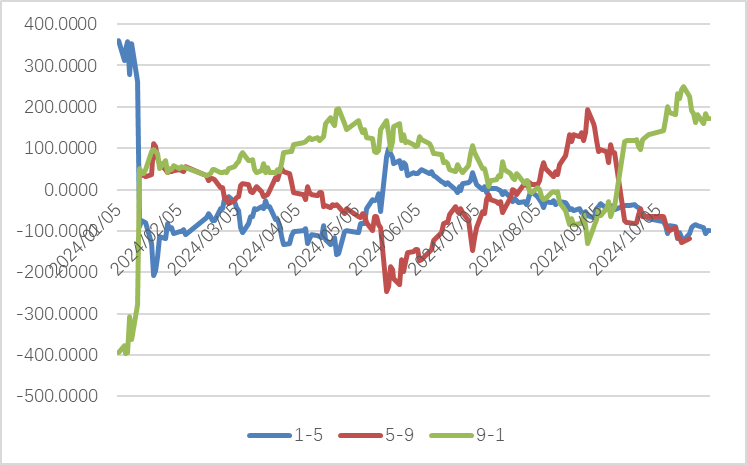

Third, the spread analysis

Judging from the current fundamental situation, glass production is facing losses in the whole industry. If the cold repair is concentrated, the profit will be improved, and the downstream will restore the willingness and ability to replenish the warehouse. The soda ash 01 contract is close to the cost line. If the market outlook sees that the inventory has stabilized and the start-up is maintained at around 80%, the far-month contract is stronger than the recent-month contract in terms of valuation. Unilateral risk is large, so it is suggested to pay attention to the 1-5 hedging strategy in intertemporal arbitrage, but at the same time, we need to pay attention to the progress of subsequent new production capacity and the capacity clearing of demand-side glass.

Figure 11: Price difference chart of soda ash-glass (RMB/ton)

Figure 12: Intertemporal price difference of soda ash (yuan/ton)

Source: Straight Flush and Huishang Futures Research Institute.

Fourth, summary of views and strategy recommendation

In the short term, driven by macro-policies, the downstream positive feedback boosted the center of gravity of soda ash to move up, and the market followed, but the improvement of actual demand was not obvious. The downstream just needed to reduce the expectation of consumption and storage, and the upstream continued the trend of accumulation. In the fourth quarter, the new production capacity was 2.3 million tons, and the supply pressure was still relatively large.

On the whole, soda ash is still in the cycle of overcapacity, and there is limited room for sustained price rebound before the fundamentals of supply and demand have improved significantly.